Intending to do the right thing doesn’t always lead to actually doing it, a tendency formally known as the “intention-behavior gap.” We can intend to go to bed early and still go to bed late. We can want to exercise and still choose not to. We can recognize the importance of saving extra money and still choose to spend it instead. So why is it so hard to change our behavior? Because, says Jonathan Corbin, Ph.D., “brains are weird” and “the world is difficult.”

Corbin is a senior behavioral researcher at the Center for Advanced Hindsight at Duke University. The Center for Advanced Hindsight recently partnered with NOVA Labs, Thought Cafè, and the Institute for Consumer Money Management to create the NOVA Financial Lab, a group of financial literacy games targeted at adolescents and emerging adults. In each game, players practice managing money while taking care of a pet. You may never have to sneak a cat into a concert or prepare a retirement plan for a dog in real life, but you will need to understand concepts like budgeting, interest, and debt. “What we hope people start to do,” Corbin says, “is really think about, ‘What decisions should I make now to make better decisions later?’”

Essentially, “Money spent now is money that can’t be spent later.” As intuitive as that might seem, “The way we think about money is relative, and it’s not linear.” When you’re already spending thousands of dollars on a car, for instance, an extra five hundred dollars for a feature you may or may not need “feels like a very small amount of money,” but in a different situation, its value can seem higher. How many times, Corbin points out, could you go out to eat with five hundred dollars?

Source: https://advanced-hindsight.com/wp-content/uploads/2022/03/CAH-NOVA.pdf

There are three games: Shopportunity Cost, Budget Busters, and Exponential Potential. (“One of the people from PBS helped us come up with these cute names,” Corbin says.) They each involve different skills, but they all focus on “financial literacy from a behavioral science perspective.” Players have to contend with both external obstacles and common behavioral biases to make financial decisions for a pet. “I always choose the dog,” Corbin adds, “but I understand other people might choose the cat.” (I chose the cat.)

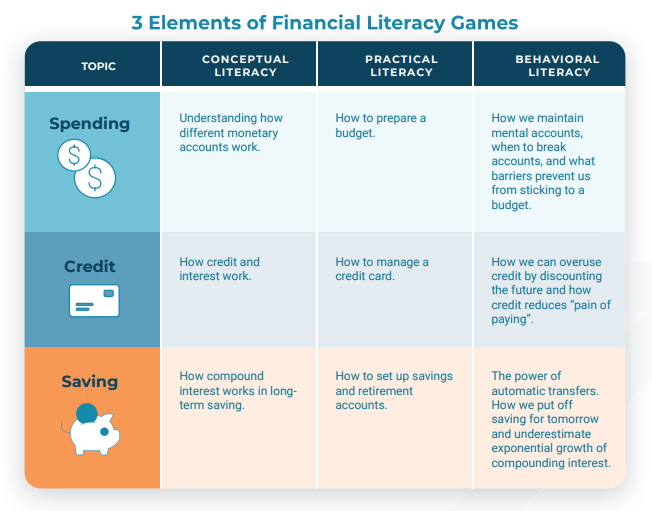

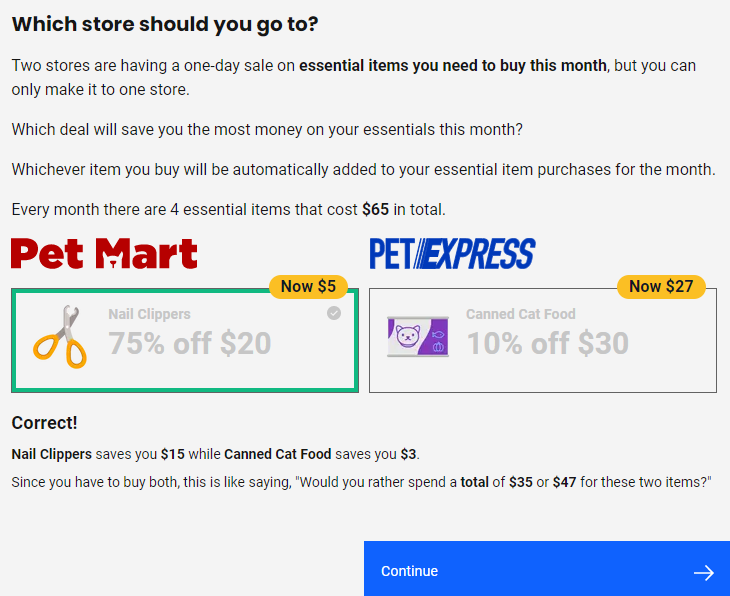

The first game, Shopportunity Cost, focuses on short-term financial planning. It involves dressing a pet up like a person in order to sneak them into a concert for the night. “You have to make decisions that optimize the pet’s happiness while also being able to make it to the concert and back home,” but you have a limited amount of money to spend. If you spend too much money too soon, you’ll run out, but if you’re too frugal, your pet won’t enjoy the evening. As goofy as the concert scenario is, it introduces players to an important concept known as opportunity cost, which refers to the potential benefits we miss out on when we choose one alternative over another. Say you’re debating between a $50 outfit and a $30 one. The opportunity cost of choosing the more expensive outfit is $20, but shoppers don’t always consider that. “Opportunity cost neglect is the simple idea that when we’re faced with financial decisions, we tend not to consider alternative uses for that money.” Reframing the $30 outfit as “a $30 dress that I’m okay with plus 20 extra dollars” that could be spent elsewhere might lead you to choose the cheaper outfit. Or it might not. “Sometimes you want the $50 outfit, and that’s perfectly fine… but a lot of the time that might not be the right decision.” Like many things, taking opportunity cost into account is a balancing act. “We shouldn’t obsess over every possible opportunity that there is,” Corbin cautions, but “consider[ing] opportunity costs can lead to better financial decisions.”

Budget Busters, meanwhile, involves medium-term planning. Players have to manage checking, credit, and savings accounts while caring for their pet over a six-month period. Along with purchasing essential and non-essential items to attend to their pet’s basic needs and happiness, players have to contend with unforeseen circumstances like medical emergencies. The game introduces people to the 50-30-20 rule, a budgeting concept that involves devoting 50% of income to essentials, 30% to non-essentials, and 20% to savings. Budget Busters also explores the principle of mental accounting, the idea that aside from formal budgets, we have “categories in our head” that change our perception of money. “Let’s say you get birthday money from your relative. That money tends to be a different kind of spending money to you than money you get from your paycheck,” Corbin explains, because “money feels different in different contexts.”

There are parallels in Budget Busters. Sometimes players receive unexpected windfalls like gifts or prizes. (My cat won $40 for being “Best in Show” at the local pet pageant.) Players get to decide whether to use the extra money on a “fun” item for their pet or put it into savings. Corbin says “gift money” is a classic example of a misleading mental account. “We tend to overspend… because it feels like it’s not even our money in a way.” In reality, though, money has “fungibility,” meaning it’s “exchangeable… across any account.” In other words, “money is money,” regardless of where it comes from. A $10 bill, for instance, can be exchanged for two fives without changing its value. (Non-fungible tokens, or NFTs, lack this property. “You can’t exchange the picture of a cat you bought from the internet for Chipotle.”) Like Shopportunity Cost, Budget Busters focuses on both traditional financial concepts and common behavioral tendencies that affect decision-making. “None of these things are necessarily bad,” Corbin emphasizes, “but they’re things that one should be aware of… when that natural proclivity may be swaying them in the wrong way.”

The last game, Exponential Potential, explores concepts like compound interest, debt, and investment. The premise of the game involves traveling back in time to balance debts and investments. The goal is to make your pet a millionaire. By showing players how investment decisions can affect future net worth, the game seeks to increase understanding of processes involving exponential growth. Exponential Potential introduces the concept of exponential growth bias. According to Corbin, “We tend to underestimate things that grow exponentially.” He cites the coronavirus pandemic as an example: “Even the people who were making the graphs of Covid’s growth… it’s really hard for them to figure out how to show that to people.” Log-transformed graphs are one option, but they can be deceptive by making the slope look flatter. Similarly, when dealing with exponential growth in the financial world, “People are going to underestimate how badly they’re going to get burned” by debt, but they may also underestimate how much they’ll benefit by saving for retirement.

With compound interest, for instance, “The interest gets applied both to principle and to interest from the last time, and that’s where exponential growth happens.” In the game, players have the opportunity to adjust how much money to put toward paying off debts, investing, and saving for retirement each month. Then they travel decades into the future to see how their decisions have affected their pet’s net worth. “We’re hoping that that kind of feedback allows you to think through… what you might have done wrong and try to correct,” Corbin says. Once again, though, raw numbers aren’t the only factor at play. “We just want people to understand what the optimal way to do this is, and if there’s a better way for them to do that psychologically, that’s fine.” Debt account aversion, for example, refers to the fact that people want to have fewer debt accounts, meaning they are often eager to pay off accounts in full when they can. Some financial advisers suggest that “because they think it’ll get the ball rolling and you’ll be more likely to pay off the next one.” According to Corbin, there isn’t a lot of evidence for that, and sometimes paying everything off at the outset isn’t ideal. For instance, “It is optimal to start thinking about retirement as soon as you can… but if you’re delaying putting money into retirement because you’re so concerned with your student loan debt,” that can be problematic. Still, Corbin understands the appeal of closing debt accounts. “I am risk-averse, which means if I have a debt I’m probably going to put more money toward that debt that I necessarily should given what the interest rates are and what I could potentially make by investing that money instead.” Financially speaking, “There’s a decent likelihood that I should just pay the minimum on my mortgage… [but] I’ve decided I’m willing to trade off those future gains for the peace of mind that if something goes wrong… I’ll be ahead on my mortgage payment.” Even in Exponential Potential, the right choices aren’t always clear-cut. Corbin describes it as a “sandbox approach” where players are given more opportunity to play around. “This is the trickiest game because there’s no perfect answer for anything,” he says. “Everything has risk.”

Another bias that can affect our financial decisions is known as present bias, the tendency to discount the future in favor of the present. Corbin offers the everyday example of staying up too late. “Nighttime Me wants to stay up and read…. Morning Me is going to be really ticked off at Nighttime Me when they’re exhausted and don’t want to get up.” Research suggests that people can have a harder time identifying with their future selves. That can easily affect our financial decisions, too. “I’m going to let future me worry about that. That guy. Whoever that is.” However, “If you can get people to identify more with that person,” they can sometimes make better decisions. Ultimately, “The game isn’t trying to force people to become investment robots.” We are biased for the present because we live in it, and that’s normal. The purpose of the game is simply “to nudge people… to worry just a little more about the future.”

“Money is basically for safety, security, and happiness,” Corbin says. The ultimate objective is to balance needs, wants, and savings to achieve those three goals both in the present and the future.